What questions should I ask when interviewing a “financial advisor”?

The unfortunate reality is that the financial services industry here in the U.S. is far from transparent. There are numerous “advisors” out there who really just salespeople looking to make a quick commission by selling you a fancy life insurance product, annuity, or mutual fund — even if it’s not in your very best interest. And it’s super hard to figure out who is who in the zoo.

Part of the problem is due to the fact that “financial advisor” is not a regulated term — which means that literally anyone can call themselves an “advisor” even if they have no formal training whatsoever.

Here are 10 questions (in no particular order) that I recommend you ask any prospective “advisor” so that you can get a better sense of what you’re signing up for and who you’re signing up with:

Question #1: With whom (banks, brokerages, insurance companies) are you affiliated? Incentives matter here. Let’s say that you need to buy a new car, so you go to the Toyota dealership and ask the representative “which car do you think is best for my situation?” What do you think are the odds that they’d ever recommend any car other than a Toyota? Or even an alternative mode of transportation like a bike, a bus, or an Uber? In the same vein, big banks and brokerages have their place, but I think that you can often find much greater transparency and service levels from independent advisors who have no ties to any particular company or product.

Question #2: Has your firm taken any private equity or venture capital money? “Show me the incentives and I’ll show you the money!” Charlie Munger wrote this and I think it’s apropos. No shade on PE, but most PE firms operate on short-term fund lifecycles with exit mandates. In my view, that timeline is fundamentally incompatible with the indefinite, relationship-driven nature of financial planning and wealth management. As an RIA owner myself, I would never want to take PE (or VC) money -- simply because I'm not willing to risk having misaligned incentives or forcing certain growth/profitability metrics at the potential expense of my clients. Worth considering: what happens when the PE/VC firm decides that they want to sell or directs the advisory firm to squeeze additional profitability out of the company? It’s most likely going to come at the expense of service levels and product offerings to clients.

Question #3: What are your credentials? There are four “core” certifications that are relevant, in my mind. They are: (1) Certified Financial Planner/CFP (2) Chartered Financial Analyst/CFA (3) Enrolled Agent/EA and (4) Certified Public Accountant/CPA. These four designations are basically the creme de la creme. It’s important to note that often (but not always), CFPs and CFAs are more proactive and “forward looking” while EAs and CPAs are more reactive and “backward looking”. A CFP is more likely to help you proactively with tax planning for the upcoming year, for example, while the EA/CPA is more likely to help ensure that your tax returns are prepared correctly after the year is already complete.

Certified Financial Planner (CFPⓇ) - The gold standard in personal financial planning, covering retirement, taxes, estate planning, insurance, and investments. Interestingly, the CFP curriculum is light on pre-IPO equity comp planning topics! So it really takes a specialist to know these details inside and out!

Chartered Financial Analyst (CFA) - Focused on investment management and financial analysis. This designation is more common in institutional finance than personal financial planning.

Certified Public Accountant (CPA) - A state-licensed accounting credential for professionals qualified to handle auditing, financial reporting, tax preparation, and compliance.

Enrolled Agent (EA) - The highest credential awarded by the IRS, granted to tax professionals. EAs hold unlimited rights to represent any taxpayer before the IRS.

Question #4: How are you paid? There’s mass confusion around this one, unfortunately, and it’s a critical question. You should ask any prospective advisor if they are “fee-based” or “fee-only”. These are not the same thing! Fee-based means that advisors may still be able to make a commission off of something that they sell you. Whereas “fee-only” means that advisors are paid exclusively by clients via either an hourly, flat-rate, or percentage of assets and act as fiduciaries. Fees that are derived from a “% of assets under management (AUM)” are generally most common for “fee-only”. Hourly rates, flat-rates, advice-only, or defined project rates are also great “fee-only” options and help to reduce conflicts of interest.

Question #5: What is my total fee in terms of dollars? Not many industries out there quote clients in terms of percentages — but I guess the financial services industry tends to be one of them (sigh). Many advisors charge “1% of assets” which sounds benign…by design. 1% of a $1,000,000 portfolio = $10,000 annually. 1% of a $2,000,000 is $20,000 annually. This isn’t to say that these fees aren’t worth it — but you deserve to understand the true cost and the services. I highly recommend that you either convert these %s on your own or ask your advisor to quote you in dollars. Then you can get a sense of whether that annual fee is actually worthwhile to you.

Question #6: Are you a fiduciary 100% of the time? Believe it or not, some advisors can actually (legally) wear a fiduciary hat in the morning and then by afternoon put on their sales hat and sell you a commission-based product. Absurd, if you ask me! To ensure that you are always getting pure fiduciary advice, ask your advisor if they are, in fact, a “100% fiduciary”. They should never be selling you a product, in my opinion!

Question #7: What documents do you request from me ahead of time? Many advisors are focused on your investment portfolio (because they charge a % fee based on that portfolio). This isn’t a bad thing per se, but if your prospective advisor is only interested in reviewing your investment documents upfront, it paints a pretty clear picture of where and how they will also be focusing their advice. In my opinion, advisors should be asking for (and looking at) tax returns, cash flow statements, equity compensation documents, and everything else that compromises a true financial plan. Investments are just one piece of the puzzle.

Question #8: How many clients do you oversee? Do you really expect to get hyper-personalized service and advice if you are one of 150 clients that an advisor oversees? And, if you’re paying based on a % of assets under management and haven’t yet accumulated a “meaningful” asset base, do you really expect to get the attention that you deserve? My rule of thumb is that if an advisor serves more than 50-60ish clients, you should naturally expect a lower service level. There are only so many hours in a day that an advisor can be attentive to all of their clients’ needs.

Question #9: How often and in what ways do we communicate? Will you be meeting in person? Zoom calls? Pre-recorded videos? Get a sense of this ahead of time so that you aren’t surprised. Also, get a sense of how frequently you’ll be meeting each year and whether you can meet if something urgent comes up (such as a liquidity event or a house purchase). Meeting twice yearly once you’re in “steady state” is probably reasonable.

Question #10: Who will be my direct point of contact? Sometimes when interviewing new clients, the advisory team will bring in their executive teams (the “top dogs”) to help close the deal. It’s literally a sales meeting for them. And during that sales meeting, you’re made to feel like you’re the most important thing since sliced bread. But then what happens all too frequently is that once the executives leave, you never hear or see them again. Instead, you’re passed to the associate advisor (who may be great), but who probably has a lot less experience and expertise. That, in turn, is not such a great feeling.

Question #11: Can you describe your typical client? Here’s a simple way to think about this: if you had a heart condition, would you rather see a cardiologist or a general practitioner? Specialists in both medicine and finance have deep expertise in unique arenas. Find someone who works with your demographic. If you have equity comp, find someone who is a specialist in helping navigate ISOs/NSOs/RSU vests and liquidity events. If you have a small business, find someone who works with small business owners. If you’re a dentist, find someone who works with dentists who have their own practice! This is the best way, in my opinion, to improve outcomes while preventing sub-optimal decisions.

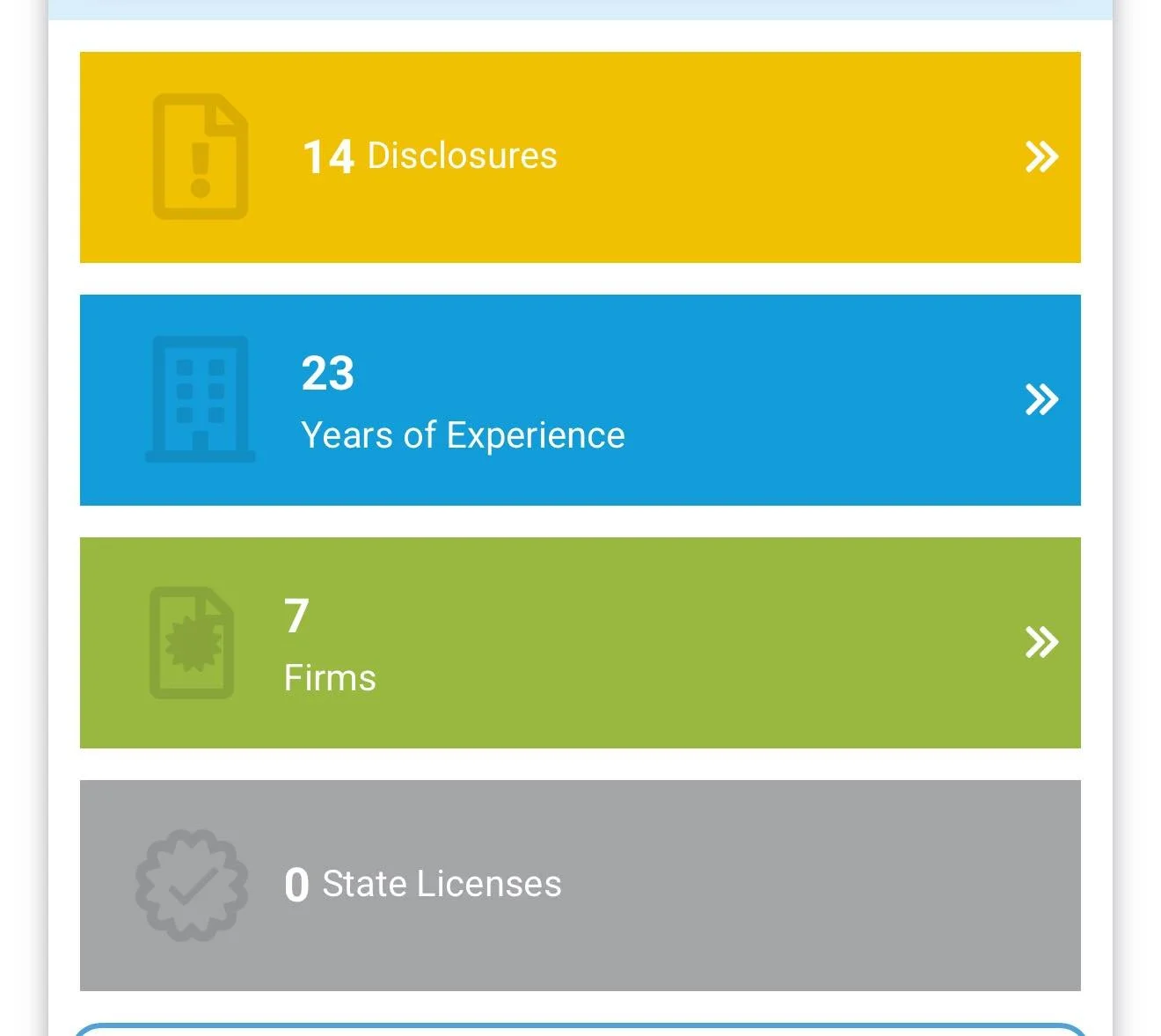

BONUS ACTION: This one is not a question but rather an action that you can take on your own to ensure that this person doesn’t have a rap sheet (known as “disclosures”). Here’s what you can do:

Go to IAPD - Investment Adviser Public Disclosure - Homepage

Search for the individual.

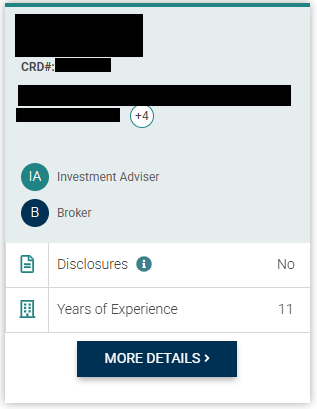

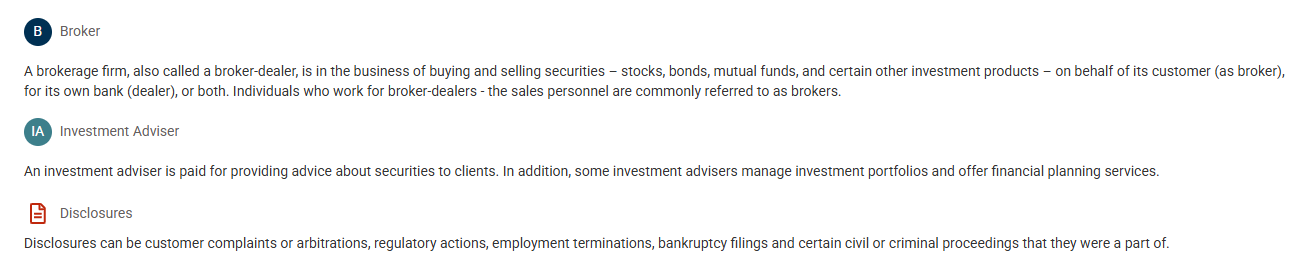

Ensure that they do not have any disclosures which would look something like this (below).

I’d also encourage you to find someone who is registered as an “Investment Advisor” and not a “Broker” to help reduce any potential conflicts of interest!