What’s the true cost of DIY-ing your finances?

I’m obviously biased, but I think that the true cost of DIY-ing is significantly more than the 0.25% or so that folks pay for a robo advisor.

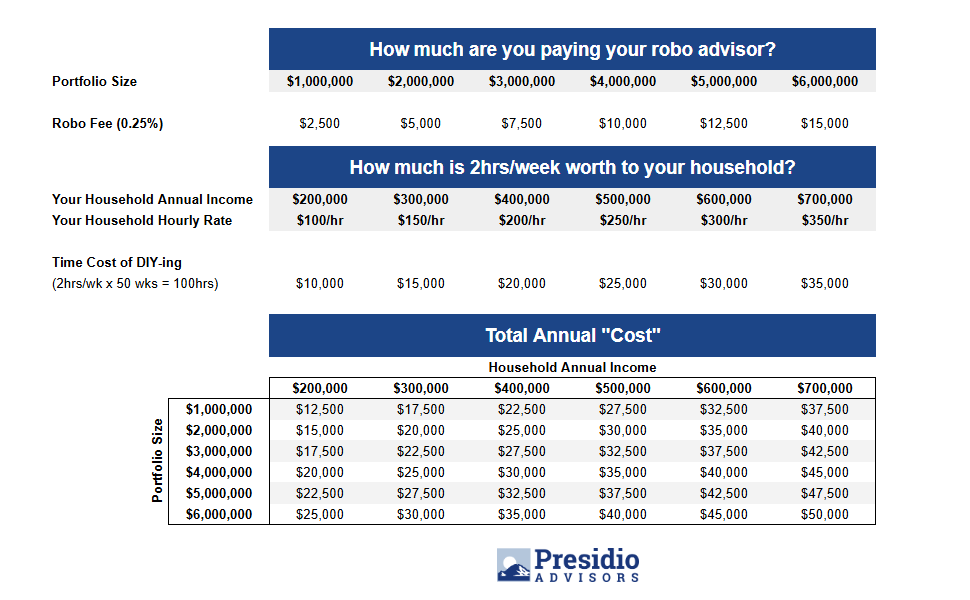

The real cost = robo advisor fee + the opportunity cost of your time.

Now don't get me wrong -- dabbling with a robo-advisor is a great way for folks to get their feet wet and I’m all for that.

But at some point, complexity + limited time + mental energy required to figure out tax strategy, equity comp decisioning, retirement analysis, cash flow projections, real estate purchases, and understanding when you can finally leave your tech job becomes…a lot. And that mental load only compounds when kids + high-stress jobs come into the picture (can personally attest to the kids part).

And then there's the question of -- after all your "research", did you even get it right??

There’s a Vanguard study suggesting that, on average, folks spend ~2hrs/wk conversing with Claude/ChatGPT or finagling things on their own. Let's assume that the study is directionally accurate.

Let's also assume that your Claude/Chat outputs are accurate…(side note: be very, very careful. I have found some crazy, basic errors and have had many “you’re right to push back!” responses).

But anyway, if you have $400,000 of household income, your time is worth roughly $200/hr. Two hours per week DIY-ing your portfolio or trying to understand our (outrageous!) tax code x 50 weeks of the year = ~$20,000 worth of TIME that you spend annually trying to figure things out solo.

Is that worth it? What could you have done with that 100 hours instead? Go to the park with your kid 100 times? Sleep an extra 2hrs/week? Have a 25 nice date nights with your SO?

Only you can answer that question.

Anyway, I put together this matrix that pairs portfolio size (assuming 0.25% robo-advisor fee) with annual household income to see what a “total cost” of DIY-ing might be for any one household.

Maybe this resonates. Maybe you think it's off the mark. Either way, I'd encourage you to figure out what your time is worth and then figure out the cost (in $) to outsource.

One last (biased) thought: I'm a big fan of small, independent advisors.

Odds are you're likely to get more personalized service, fewer conflicts of interest, and less likely to feel like a cog in the machine. Let me know if you need some resources on where to look and what questions to ask.

I think that most people forget to incorporate the cost of their time when they look to DIY their finances.