Considerations when participating in your company’s tender offer

I help Millennials and tech professionals with their equity compensation. And I frequently get inbound requests for “help!” when a company is announcing a tender offer or filing their S-1 paperwork in preparation for an initial public offering (IPO). That’s when most employees realize “oh, crap! I have a bunch of vested equity, but I haven’t done anything and have no idea what it means or how to optimize it.”

Don’t worry – I’m used to the burning timelines, and this stuff is my bread and butter, so I’m happy to help 😊.

Today’s blog post highlights what happens within a tender offer and the common implications, pitfalls, and clarifying questions to ask your company so as to avoid any tax surprises.

At a high level, the type of tender offer that I’m referencing here is an opportunity for employees at private companies to cash out on some of their vested equity. This is a really, really good thing since there generally is no liquid, tradable market for private-company stock — and certainly no guarantee that there ever will be. Most employees don’t realize how rare it is for a company to have any sort of liquidity event — be a tender offer, acquisition, or IPO (the odds of any liquidity are generally less than ~7% or so).

So the opportunity to take some chips off the table — presumably at a price that has economic benefit to you (the employee/common shareholder) — should be welcomed with open arms.

Companies also view tender offers favorably in that they believe tender offers 1) generally improve employee morale and retention by de-risking the amount of concentrated equity that employees hold 2) allow investors to cash in on their investment which 3) thereby reduces the pressure to generate liquidity by going public and 4) allows the company to choose the price to sell and to whom they sell. A win-win for employees and companies.

But the innerworkings of a tender offer from one company to another are rarely similar. Each one is unique and the devil is in the details. Which makes things both fun (for me, as a tax strategist, at least) and uniquely challenging. That’s because:

1. There is no set playbook for a tender offer. Each company chooses their own adventure in the sense that each company decides:

Who is eligible to participate? Just current employees or are former employees eligible?

How many shares can be sold by each participant? 20%? 25%? 25% plus X% up to a certain threshold?

What about vested options? Are they eligible?

Can vested options be “cashless exercised” or must they be exercised prior to the tender?

Are vested RSUs eligible for participation? What happens if they are double-trigger RSUs?

2. US tax law, perhaps because of or despite its complexity, is surprisingly “gray”. As in, there is so much “gray zone” around the tax laws that impact tender offers that each company’s tax and legal team often has their own various interpretation of how to mark the transactions on their books. Which also means that it’s imperative to get clarity from the company on how to interpret these different clauses.

The only problem is that companies don’t want to muddle into giving any sort of “tax advice” which also means that they can be exceedingly unhelpful is getting answers to basic clarifying questions.

For the record – as an Enrolled Agent (which is the highest designation awarded by the IRS), I love giving tax advice. That’s literally what people pay me to do! So, yeah, ask me all your tax advice questions.

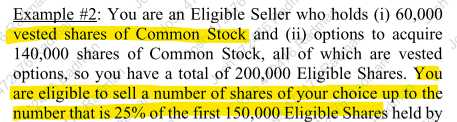

The following screenshots exemplify the potential “gray zone” of tender offer taxation and why company interpretations matter. In this case, it was imperative for my client and I to ask the company for clarification on how we should proceed with our interpretations.

Interpretation: Employees can exercise their ISOs (a disqualifying disposition), but if the option shares aren’t purchased, then they lose their tax-advantaged status and automatically convert into NSOs.

“Gray Zone”: Does the entirety of the ISO grant convert to NSOs (rather than just the vested option shares that were offered as part of a Contingent Exercise)?

Potential taxation impact: This should be relatively straightforward. In theory. The reality is that some companies will convert not just the option shares you offered during the tender, but rather convert the entire grant to NSOs – which is a huge deal! I’ve seen it happen!

Interpretation: The most recent 409a/FMV has been updated to reflect the tender Offer Price.

“Gray Zone”: In contrast to what is listed in the tender offer documents, the most recent 409a/FMV was listed as $X whereas the Offer Price in the tender is $X + $40. There are big implications if the incremental $40 is taxed as long-term capital gains or as compensatory income, and we need to know how to account for that!

Potential impact: A higher 409a/FMV can be double-edged sword. On one hand, for those who are selling common shares within the tender offer, it could mean that more of your qualifying ISOs are taxed at long-term capital gains. But on the flip side, for those who have not yet purchased all of their equity, it could also mean that purchasing your option shares just got a lot more expensive. Now you have a much greater bargain element, which can increase your Alternative Minimum Tax (AMT) liability and/or ordinary income tax liability.

Interpretation: Common Stock can be sold within this tender offer.

“Gray Zone”: Are RSUs considered Common Stock within this tender offer?

Potential Impact: If this tender offer allows for RSUs to be sold, there are much broader implications around how RSUs will vest and, consequently, be recognized as ordinary income to you, the employee.

All of this is to say that tender offers are complex. They’re nuanced. They require precision planning and tax strategery. If you’re lucky enough to work at a company that provides a tender offer and need help or a second set of eyes, feel free to reach out.

Good luck!

-Josh